Is That Dream Life a Blessing or a Burden? 🏠🚗✈️📚💭✨

Let's be honest — who hasn't thought about living their dream life? Picture this: a cozy home with a balcony for lazy chai mornings, a plot of land for future ventures, a shiny new car in the driveway, beach vacations on your calendar, and your kids' education fully funded. Sounds perfect, right? 🌿🚙🏖️🎓

But before you get swept away by glossy brochures and tempting deals, let's take a closer look at how chasing all these dreams together could reshape your financial story. 📉💸📊

I've built a custom Excel sheet — not your average snooze-worthy tracker, but one that mirrors your real-life money flow. 🗺️📈🔍

So, why go through the effort when the market is flooded with free and even paid templates? 🤔💭 Because frankly, most templates oversimplify the process. They either spit out how much more SIP you need to pump in monthly 📈💸, or they assume blanket withdrawals without considering crucial realities — like taxation, liquidity, goal-specific impact, or how every financial decision influences your entire net worth. 📉⚠️

What I really wanted was clarity: When exactly might my corpus dry up? How would big goals — whether it's a house, a shiny new car 🚗, a dream vacation ✈️, or my kids' education 🎓 — shape my long-term wealth picture? And how can I withdraw intelligently without unknowingly derailing everything?

Unfortunately, none of the ready-made calculators gave me that depth and precision. If you've seen one that does, do let me know! 😉

That's why I rolled up my sleeves and built this tracker — first to satisfy my own curiosity, now so everyone else can explore it, tweak it, and maybe even improve it. 🎯🚀💼 Here's how it works:

- 🪙 Step 1: Get crystal-clear visibility of your monthly expenses: Needs, Wants, and Savings.

- 🛡️ Step 2: Ensure your financial safety net is foolproof — review investments, liabilities, and upcoming goals.

- 📊 Step 3: Analyse your financial health to see how long your money can carry you forward.

- 🏠 Step 4: Finally, answer the biggie: Can you genuinely afford that dream property?

We covered Step 1 in Chapter 1 and touched on financial safety nets in Chapter 2. Now, it's time to channel your inner money wizard and forecast your future. 🔮💼📅

Meet Rahul — The Spreadsheet Star 🌟📊🔥

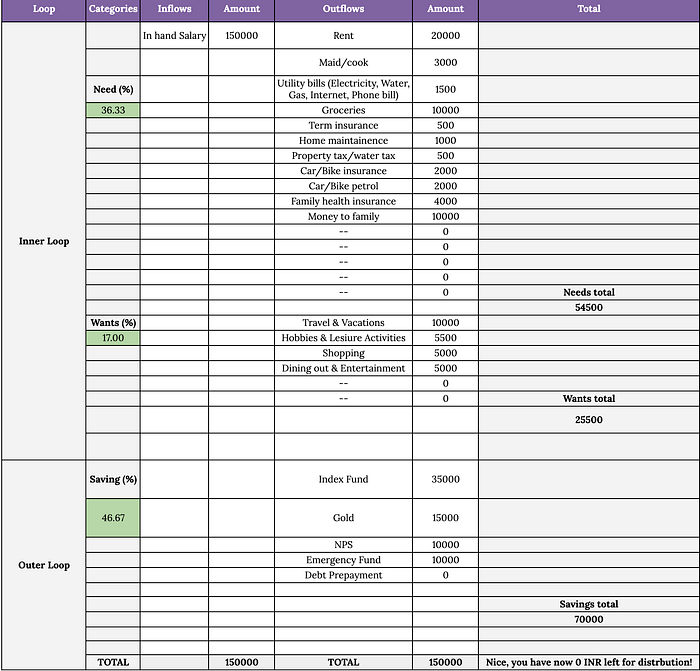

Say hello to Rahul. 25 years young, pulling in ₹1.5 lakh/month in-hand salary. Living the DINK (Double Income, No Kids) dream, but with razor-sharp financial discipline. I will explain all the flows with screenshots from excel sheet. Here's how his money flows: 🏃♂️💸✨

- 💳 Needs: ₹54,500/month — Rent, groceries, bills, petrol — life's basics.

- 🎉 Wants: ₹25,500/month — Netflix binges, weekend getaways, shopping sprees.

- 💰 Savings: ₹70,000/month — A jaw-dropping 46% savings rate! (Seriously, round of applause.)

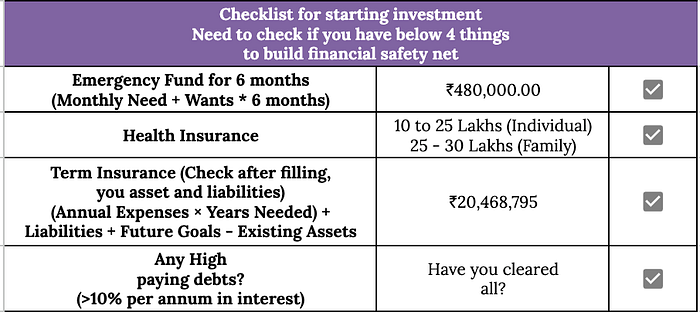

But wait, Rahul's not just winging it. His financial safety checklist is on point: ✅🛡️📋

✅ ₹5 lakh Emergency Fund stashed in small finance banks (hello, better interest rates!).

✅ ₹10 lakh Health Insurance — one hospital visit won't drain his savings.

✅ ₹1.7 crore Term Insurance — calculated with precision.

✅ Zero high-interest debts lurking in the background.

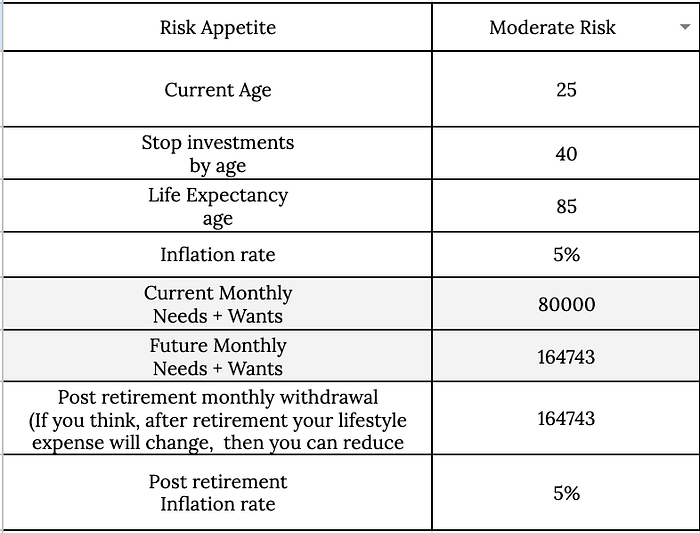

His master plan? Invest aggressively until 40, retire from investing, and let compounding work overtime till he's 85, ideally sipping coconut water by a beach. 🌴🍹📊

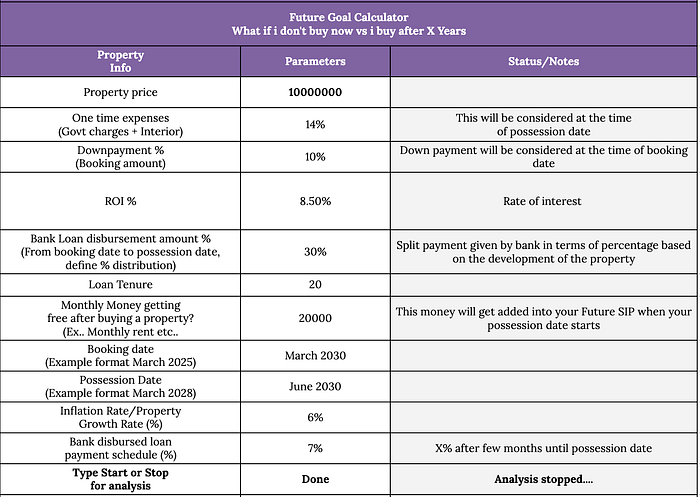

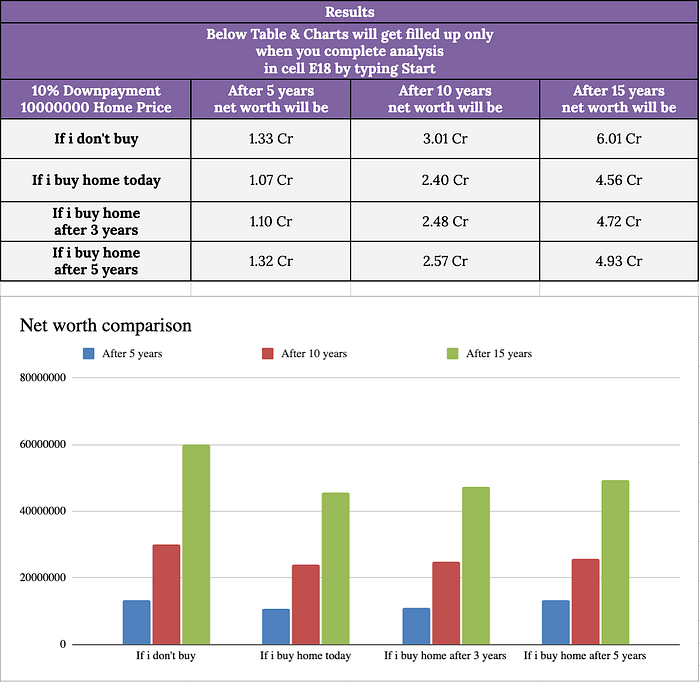

Can Rahul Afford That ₹1 Crore Dream Home? 🏠💡🎯

Before we dive deeper into Rahul's financial journey, here's the juicy part upfront — the result! 🎯📢📊

Using Step 4 — Goal Affordability Calculator, Rahul ran multiple scenarios:

- 📅 Should he buy property NOW or wait 3 or 5 more years?

- 🔢 Tweaked factors like down payment %, loan tenure, interest rates, and property appreciation.

👉 If Rahul makes a 50% down payment (~₹50 lakhs) today, he'll wipe out 85% of his liquidity which is Not ideal! 🚨📉⚠️

But if Rahul plays it smart:

- 💡 Starts with just a 10% down payment.

- 📈 Keeps the rest invested, earning ~12% returns.

- 💸 Lets the investment growth help shoulder EMI payments.

Better still, if he waits 5 years, his net worth could balloon by ₹40–50 lakhs more! 🚀💰🎯

Quick heads-up: The outcome shifts based on your existing investments. Lesser investments = bigger interest burden, potentially dragging your net worth. ⚖️📊🔻

Now, let's rewind and break down how Rahul arrived at these numbers… ⏪📈🔍

Can Rahul Really Afford That ₹1 Crore Home? Rahul's Current Investments 💼💹📊

- 📈 ₹30 lakhs in index funds

- 🪙 ₹5 lakhs in Gold ETFs (because why not hedge!)

- 🏦 ₹15 lakhs in EPF

- 🏛️ ₹5 lakhs in NPS

- 💼 ₹5 lakhs in Emergency fund

Each row lays bare returns, taxes, liquidity — no fluff, just facts. It even projects how fat his portfolio will look post-40. 📊📉🔢

Monthly SIP Contributions: 💸📅💼

- 📈 Index Funds: ₹35,000

- 🪙 Gold: ₹15,000

- 🏛️ NPS: ₹10,000

- 💼 Emergency Fund: ₹10,000

Future Lumpsum Bonuses: 🎁💰

April 2026 brings a ₹1.5 lakh bonus. He has already earmarked — swooshing straight into equity mutual funds, with projections stretching 15 years ahead. 🔮📊📆

Financial Goals 🎯💡💰

- 💍 Wedding: ₹25 lakhs in December 2028 (inflation adjusted).

- 🏠 Dream Home: ₹1 crore property.

But how does he fund these without crushing his investment momentum? 🤔💸⚡

In Excel Sheet, Withdrawal strategy is Simple, but tactical: 📝📊🔍

- 💧 Dip into Highly Liquid Investments first.

- 💼 Next, Moderately Liquid Investments.

- 🔒 Still short? Break into Lock-in Investments.

- 🏚️ Absolute last resort: sell Illiquid Assets.

Every withdrawal neatly accounts for tax implications. No fantasy numbers — only reality checks. ✅📉🔢 There is still more work to do for Illiquid taxation but we will come to that later again.

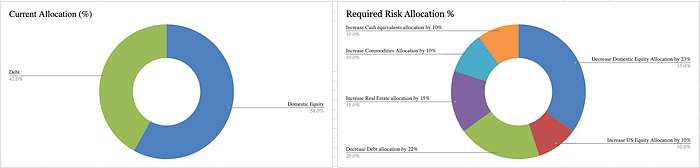

Risk Allocation Reality Check 🔄📊⚖️

Based on his moderate risk appetite, Rahul fine-tunes his asset allocation. The sheet even gives him gentle nudges when it's time to rebalance. 🛎️📈📊

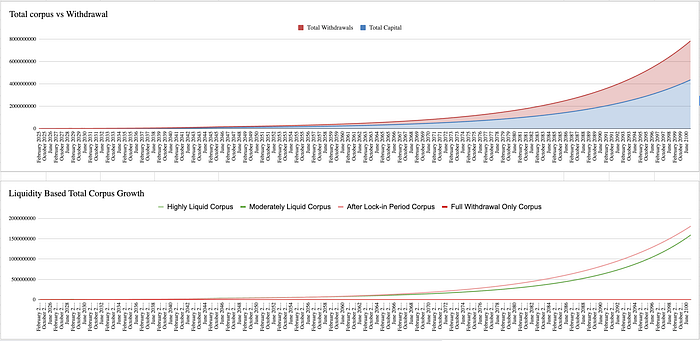

Bonus: Visual graphs show how his wealth builds — and how those goals nibble at his investments over time. 📊📉🎯

Rahul's Net Worth Trajectory 📈💰🚀

- 📊 Today: ₹60 lakhs net worth.

- 🚀 Age 40: Estimated ₹6 crores.

- 💹 Age 85: A jaw-dropping ₹198 crores! (Of course, life might throw a few curveballs — think kids' education, flashy cars, or mid-life crises.)

This is without accounting for several future financial goals.

With the home loan factored in, it appears Rahul will need to continue his aggressive investing strategy for an additional 6 years beyond age 40. Stopping at 40 would see his corpus deplete earlier, falling short of supporting him till age 85. 🚨🗓️📉

Here's how things stack up finally:

- 📊 Today: ₹60 lakhs net worth.

- 🚀 Age 46: Estimated ₹9.37 crores.

- 💹 Age 85: ₹46 crores still intact! (Still life's big surprises — kids' education, new cars, vacations are yet to be covered..)

The Moral of Rahul's Story 📝🏆💡

Buying property isn't about FOMO or flexing on Instagram. It's about playing long-term chess with your money, ensuring each move today ripples positively over decades. 🧩💰⏳

But more importantly, it's about understanding your unique financial journey. Rahul's numbers and outcomes are a starting point — what happens when you plug in your own salary, expenses, investments, and goals?

Maybe you'll find that a few small tweaks — like trimming wants, adjusting SIPs, or delaying a big purchase — can dramatically change your wealth trajectory. 📊💡🚀

Here's the fun part: My Excel sheet isn't static. It's built to be flexible:

- Add your future goals, like travel, education, early retirement, or big-ticket items.

- See how tax, investment type, and timing affect your cash flow.

- Test "What if" scenarios. What if you get a bonus next year? What if you cut back on EMIs?

Every click gives you better control over your money. 🎯📅💰

Ready to run your own numbers? Make a copy of the sheet and check where you stand. 🚀📈💭

Some of you may discover you're already financially free, while others might get the nudge they need to act now. Go ahead, give it a try, and feel free to share your feedback or questions in the comments below. 💬📩🙌

Heads-up: Since the Excel sheet is freshly built, you might stumble upon a few bugs here and there. 🐞R🔧RFel free to share any issues or suggestions — it'll only help make it better! 🚀😊

#PersonalFinance #BudgetingTips #MoneyManagement #FinancialFreedom #TrackYourExpenses #WealthBuilding #InvestmentStrategies #SavingMoney #FinancialPlanning #MoneyMindset