THE RULES OF MONEY ARE SHIFTING FAST

In this story, I am sharing so many ways to build your net worth fast in 2026.

I'm confident today that if you're able to even implement just one of these strategies, your net worth will grow.

1. The 1% Rule

Let's get into number one today, which I call the 1% rule. One of the fastest ways to build your net worth is simply to reduce the amount that you spend on discretionary purchases. And this is where the 1% rule comes in.

It states that you should think twice about any discretionary purchase that is more than 1% of your net worth.

So, if your net worth is $20,000, you want to think twice before making any purchase that is around $200 or more.

If your net worth is $50,000, then any purchase that is $500 or more, you should think twice about it, and so on.

The less money you spend on discretionary purchases, the more you can add to your investments to actually grow your net worth fast.

If you have a net worth of $20K and you make a $200 purchase or 1% of your net worth every single month, that's the equivalent of $2,400 per year.

But every year, of your net worth, that's 12% of your net worth. This same habit over the course of 40 years could cost you $671,474 over the course of your entire career.

And I think that's pretty crazy. This 1% rule is important when you're under $100,000 in net worth because, as you know, most of the friction in building your net worth is going to be at the beginning of your journey.

Eventually, as your net worth passes $100,000 or $200,000, we can relax this rule a little bit and spend a little bit more freely.

But hopefully by the time you reach $100k, you will have ingrained a habit of really thinking twice before any big purchase.

In general, I like to wait a week or even up to a month before committing to a big purchase because time will really reveal to me if I really want that prospective item or not.

2. Disconnect Your Time From Your Earnings

If you really want to increase your net worth a lot this year, try to pursue activities and careers that pay you based on how well you perform and not your time.

So, words from Naval RaviKant and what he has to say.

The first thing, if you're going to make money, is that you're not going to get rich renting out your time.

Even lawyers and doctors who are charging three, four $500 an hour, they're not getting rich because their lifestyle is slowly ramping up along with their income, and they're not saving enough; they just don't have that ability to retire.

So the first thing you have to do is you have to own a piece of a business.

You need to have equity either as an owner, an investor, shareholder, uh or a brand that you're building that accrues to you to gain your financial freedom.

So there are two things that Naval is saying here.

- The first is that you have to keep your lifestyle in check because he sees doctors and lawyers who are earning $300 to $500 an hour and actually not accumulating wealth. Now, this topic of avoiding lifestyle inflation and living below your means is one of our points for later on in this story. So, we'll dive into that more a little bit later, so stick around for that.

- The second argument that Naval points out is that in order to get wealthy and increase your net worth fast, you actually need to have some sort of equity, as he likes to call it.

In other words, you won't get rich renting out your time. He says that you need to own a piece of a business, but I think that as long as you have a career or activity that pays you a percentage based on how big the deal or how successful you are, then I think that's a really great way to grow your net worth very quickly.

So, just to give you an example, a realtor makes commissions on real estate. So, the more expensive homes they sell, the higher the percentage that they take home.

So often, the work done to sell a multi-million dollar house, say a $3 million house versus a $1 million house, is likely very similar, but the results are going to be vastly different for that realtor.

The trade-off is often that these types of jobs require you to be intrinsically motivated, and that's not something everybody has.

So you really have to know yourself in these situations and know if you can be a self-starter or not.

You could theoretically still increase your net worth by working a high-paying job on an hourly basis, like being a doctor or a lawyer.

But if you really want to increase your net worth fast, you're going to have to find a job that disconnects your earnings from your time.

3. Invest Any Bonus or Windfall Money

So throughout life, for example, you will come across windfalls or bonuses.

That could be at your job, you could get a bonus, you could get an inheritance, a tax refund, or, through some stroke of luck like the lottery, you might win a lump sum here and there.

When these types of events happen, the best thing that you can do is to pretend that money was never there to begin with and just drop it all into investing. In practice, this is a lot easier said than done.

And I would wager that 99% of people who get a bonus or a tax refund of $5,000, they'll want to spend some of it.

So instead, I think a realistic go-to would be to take 10% of whatever windfall is coming your way and treat that as your fund, spending money, and then invest the remaining 90%.

That way, at least you're benefiting from getting your bonus money.

It's still a good compromise here because the majority of it is still going away towards your future self, but at least you get a little bit of money to play with.

To illustrate how powerful this is, imagine you get a tax refund of $3,000 every single year, and you're able to invest 90% of it.

So, $2,700 over the course of even just 20 years. That can compound to an extra $133,000.

All from being disciplined when you get that windfall. So, make sure to do that.

4. Grow Your Income Faster Than Your Expenses

This one might be a little bit too self-explanatory, but I think there are two main ways that you're going to build your net worth fast.

The first is to have a higher income while your expenses stay the same.

Number two, you want to have the same income while your expenses go down.

In both cases, you are increasing the gap between what you earn and what you spend.

So there are actually three practical ways that you can do this today.

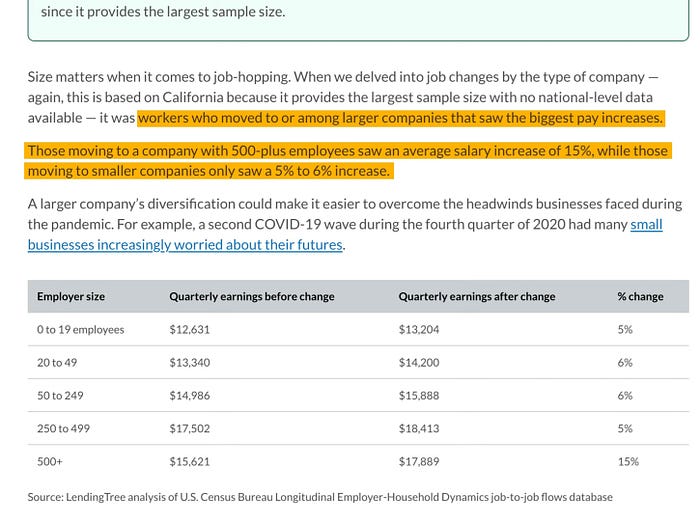

First is going to be job-hopping strategically.

According to Lending Tree, quote, "When workers moved to larger companies, they saw the biggest pay increases. Those moving to a company with 500-plus employees saw an average salary increase of 15%, while those moving to a smaller company saw a five to 6% increase. In both cases, if you switch jobs, you seem to get an increase in your pay."

And sometimes I think that if you stay at a company for too long, the pace at which your raises actually happen to you or occur to you slows down quite a bit.

The problem is that companies aren't incentivized to pay you market rate once you're already there.

So, if you want to think about it from the company's perspective, you're already doing the work.

You've already said yes to the salary. So why would they voluntarily give you a massive raise to match market rates?

Now, here's the thing. The market rate for your job could be 20% to 30% more than what you're making right now.

And when they hire someone new, since there's no salary transparency these days in all of corporate America, you could have a situation where a new hire is making 20% more than you, and you've been there already for, let's say, 5 years.

This is why job hoppers often come out ahead financially, because when you interview for a new job, you're negotiating from a market rate and not your current salary.

The second way you can increase the gap between your income and expenses is to aggressively cut the expenses side.

This requires a little bit of tracking and planning. But if you can write down all the categories in which you spend money, assess where you're spending too much, and ruthlessly cut all of those expenses in that overinflated category, that is another great way to bring your expenses down while your income stays the exact same.

And the third way is to build a high-value skill to increase your income over time.

These are going to be skills that directly increase and generate more revenue for your company or skills that are in really high demand, but there aren't a lot of people doing them.

I've seen people go from 60k a year to 120k a year by learning data analytics or SQL, which is a programming language, in order to manipulate data.

If you're a tradesman, you could increase your skills by learning to weld, HVAC, or even electrical work.

And I've also seen people just have an incredibly lucrative side hustle by learning video editing or digital marketing.

This is a little easier said than done, but if you're able to spend 6 to 12 months dedicating evenings and weekends to learning a high-income skill, it's another great way to increase your income.

5. Track Your Net Worth

67% of Americans say they don't currently track their net worth, according to Credit Karma.

And I think that being aware of your net worth is an easy win and easy way to grow it fast, because I find that the more energy and attention you put into your net worth, the more it naturally grows.

So, to calculate your net worth, you just add up all your assets and then subtract any debts or liabilities, and boom, that is your net worth.

6. Control Your Lifestyle Velocity

So, what does that actually mean? It means that when you have the momentum of increasing your income every single year, that's when it's very easy to increase your lifestyle, and when you should keep it in check.

Let me just list out a few crazy statistics of large expenses.

The total cost of owning and operating a new car is $11,577 from AAA.

The average annual cost of owning and maintaining a home in the US is $21,400 in 2025, according to Bank Rate.

And the average cost of a vacation is now $7,249, according to travel insurance provider Square Mouth. And if you want to go overseas, make that $9,922.

Lifestyle inflation occurs because, as we make more money, we think that buying more goods and services is going to bring us more joy and happiness.

But unfortunately, you may or may not know this already.

What actually happens is that buying new things doesn't necessarily always increase your satisfaction and happiness in life.

True fulfillment often comes from meaningful experiences rather than buying new things.

So I would say focus on experiences. Control your spending when it comes to your lifestyle and delay status purchases as much as you can, and I think your net worth will thank you.

7. Maximize Your Tax Efficiency

This method is all about keeping significantly more of every dollar that you make without having to earn more money.

There are three main ways to do this, in my opinion.

The first is to max out your 401k employer match and use your retirement accounts strategically.

For 2026, the 401k limit is now $24,500 per year if you're under the age of 50 or 32,500 if you're 50 and older.

For an IRA, it's $7,500 under the age of 50 and $8,600 per year over the age of 50.

Contributing to a traditional retirement account is tax-deferred. So, that means it lowers your taxable income for the year that you contribute to them.

The second strategy is to use the retirement accounts to actually shelter your investment gains from taxes as long as possible.

Every time you realize a gain by selling a stock in a taxable brokerage account, you will have to trigger and pay capital gains taxes.

But inside a 401k or IRA, you can buy, sell, and rebalance without any immediate tax consequences.

And over time, this compounding can make a huge difference in your net worth.

Also, you get some bonus points if you invest within a Roth IRA, where the earnings grow tax-free.

And the third method for tax efficiency is to tax loss harvest in your taxable accounts.

If you have investments that are down in their positions, so that they're negative, you can sell them to realize losses, and that can offset some of your realized gains.

Then, what you can do is just immediately buy a similar investment to maintain your market exposure and your asset allocation.

And this strategy allows you to reduce your tax bill, thus saving you money overall and still increasing your net worth.

So make sure to take advantage of the tax efficiencies allotted to you.

8. Negotiate Everything

I didn't know that you could do this, but you can negotiate for a lot more things than you think in life.

I personally have a friend who used to take negotiating to the extreme and would try to negotiate at the butcher shop when he was buying steaks and fish.

His rationale was, well, if they can't sell certain cuts of meat by a certain time, they'd probably rather discount them and sell them rather than having to throw them away.

And to my surprise, it actually works for him at least some of the time. And that's what he told me anyway.

Now, that's pretty extreme. We don't need to be negotiating on a New York strip at the butcher shop.

But we can still be negotiating things like your salary, your utility bills, home repairs, wedding vendor costs, etc.

There are two main things to know about negotiating, though.

Number one, it is very, very uncomfortable, but it can be worth a lot of money.

If you start a new job and negotiate your salary to be $5,000 higher than the initial offer they give you, and then you do nothing at all, but you get a 3% standard raise every single year, that one conversation was worth $59,000.

And the second thing that you should know about negotiating is that negotiating for anything is done all the same way.

You must figure out what you want, what you're willing to accept, and then figure out what you're going to do if your negotiation fails.

I'm going to link this Reddit thread that teaches you exactly how to negotiate step by step, and it's definitely worth reading if you're thinking about negotiating for anything in life.

Now, I've personally saved $600 to $1,000 per year just by making a few 15-minute phone calls to my different utility and insurance providers.

In my case, last year, it was on auto insurance, but you can also save money on other bills by calling companies and simply asking.

A lot of companies will have retention departments whose entire job is to keep you as a customer, and they have discounts that they can offer, but you have to ask, and it costs you nothing to ask.

So, make sure you at least ask.

9. Automate Literally Everything

Most people fail at growing their net worth because they make decisions too often.

You can avoid all of this if you just literally automate everything. So, set up automatic transfers so that when your paycheck hits your checking account, it gets automatically divvied up into other places that you might need it to go.

Say you get paid twice a month, and you want to save $500 per paycheck. You can set up an automatic transfer from your checking account to your investment account for $500 on the day after each payday.

That way, the money is gone before you have a chance to spend it on anything else.

The psychology here is straightforward. You can't spend what you don't see, and you're not relying on discipline or remembering to invest every paycheck.

It just happens automatically. Here are the top five things to automate.

In my opinion:

- Your Utilities

- Your Rent or Mortgage Payments

- Credit Card Bills

- Savings Transfers

- Investment Contributions

Automate your money into those five buckets and then thank me later when your net worth has grown.

10. Increase Your Financial Literacy

You can do this by reading the guides on my profile. You could read books, you could listen to podcasts, or just go through any content that you can find on the subject of personal finance and investing.

The ROI when it comes to increasing your financial literacy is essentially infinite because one good book or even one good habit that you learn from a book can snowball into good decisions, which snowball into more wealth as time goes on.

Financial literacy can compound better than money, in my opinion, because each concept that you learn will build on the previous one that you had before.

If you understand compound interest, for example, this emphasizes starting early.

Understanding tax efficiency means that you can structure your investments or your businesses better.

Understanding psychology or the behavior of finance will help you with decision-making in the long term.

Most of this knowledge is free, and that's the beauty. You don't want to ever pay a boatload of money for financial education, as I learned a lot of what I know for free online.

People who build wealth are just the ones who make better decisions with what they have.

They aren't necessarily the ones who earn the most money.

So, I think you should invest in your financial education because it's the one investment that's guaranteed to pay dividends for the rest of your life.